XL4J Tutorial

Getting started

Pre-requisites

You can build XL4J Add-ins on any operating system that supports Java: you do not need Windows or Visual Studio unless you want to modify the native parts of the Add-in, which is unlikely for most users. Being able to build from Linux or MacOS can prove very useful later on for e.g. continuous integration, but given that you’re likely to want to test and use your Add-in in Excel, it is probably advisable to start development there. Windows 10 is recommended, but any version of Windows later than Vista (7, 8, 8.1, 10, 10 Anniversary Update) should be fine.

You will need to install a current JDK and a version of Maven after 3.1. You should also have a git client installed. I would suggest using the Chocolatey package manager, which can install these packages for you using:

choco install jdk8 maven git

but it’s fine to just download and install them yourself too. You’ll probably want your favorite IDE too. If you want to be able to actually test your Add-ins, you will probably want to install Excel too! Any version after (not including) Excel 2007 is fine.

Note that you MUST have a 32-bit Java runtime (JRE) installed for XL4J to work. I have found Chocolatey can be a bit hit and miss at installing this correctly, so I’d recommend downloading the i586 version of the JRE yourself and installing manually.

Cloning the template project

We’ve provided a template project that you can use to get started. It’s very basic, and just consists of a Maven POM which pulls in the required libraries and a Maven assembly plug-in manifest which describes how to package the resulting Add-in into both a directory (so you can use it directly) and a zip file for distribution.

Start by cloning the project:

git clone https://github.com/McLeodMoores:xl4j-template.git

Inside you’ll find a standard Maven project layout. Now is a good time to import this project into your IDE of choice, or fire up a text editor.

Adding a new custom Excel function

Try adding this class:

package com.mcleodmoores.xl4j.template;

import com.mcleodmoores.xl4j.XLFunction;

public final class MyFunctions {

@XLFunction(name = "MyAdd", description = "A simple function", category = "XL4J")

public static double myadd(

@XLParameter(name = "One", description = "The first number") final double one,

@XLParameter(name = "Two", description = "The second number") final double two) {

return one + two;

}

}

Build the Add-in

Then build using:

mvn install

This will pull in the required libraries and produce the build artifact. Have a look in xl4j-template\target and you should see two

files:

- A folder called

xl4j-template-0.0.1-SNAPSHOT-distribution - A zip file containing that folder called

xl4j-template-0.0.1-SNAPSHOT-distribution.zip

Manually add the Add-in to Excel

- Start Excel.

- On the Backstage (the screen revealed by clicking on the

Fileribbon header or Office button), choose Options. - Go to

Add-ins - Next to the dropdown list towards the botton called

Manage:, selectExcel Add-insand clickGo. - Click

Browse, navigate to thexl4j-template-0.0.1-SNAPSHOT-distributionfolder, open the folder containing the appropriate distribution and select the add-in. - Click

OK. You should see a popup and a splashscreen once you’ve clickedOK. -

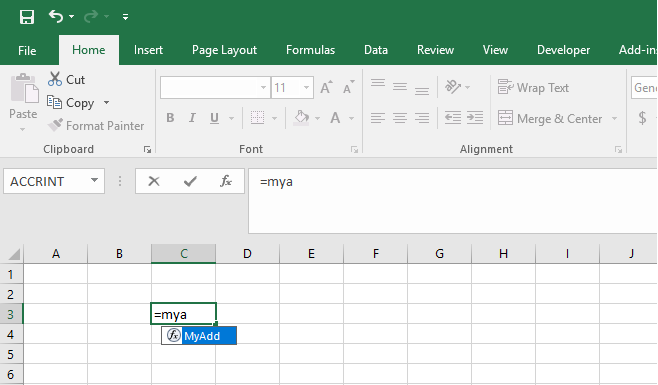

Start typing in your function name. Excel will autocomplete the name:

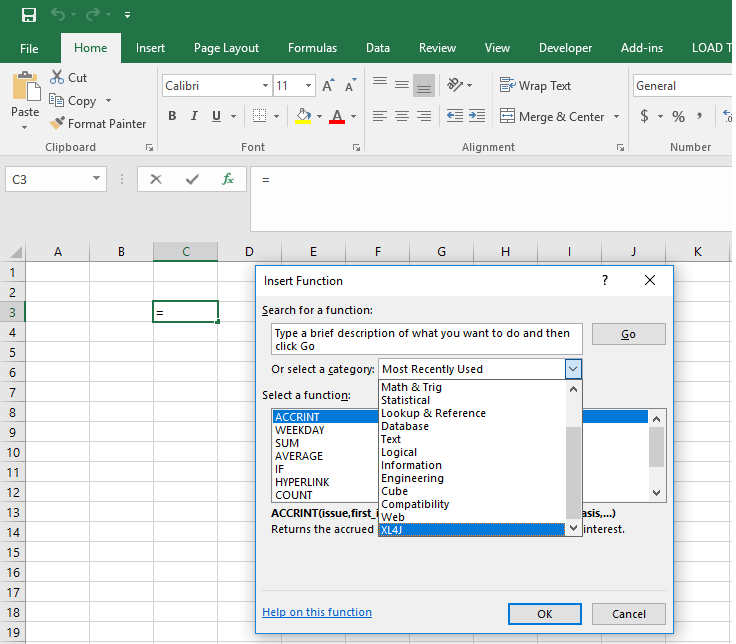

Or you can use the function wizard:

TODO add an image of the argument wizard when it’s fixed

Using Java projects from Excel

A simple wrapper

In this example, we are going to write a layer that allows the to be used from Excel. To get pricing and risk metrics, we need

- A yield curve

- A CDS curve

- A CDS trade definition

Just for reference, here is some example Java code that constructs a yield curve using the starling library:

/** The trade date */

private static final LocalDate TRADE_DATE = LocalDate.of(2016, 10, 3);

/** The quotes */

private static final double[] QUOTES = new double[] {0.001, 0.0011, 0.0012, 0.002, 0.0035,

0.006, 0.01, 0.015, 0.025, 0.04};

/** The money market day count */

private static final String MONEY_MARKET_DAY_COUNT = "ACT/360";

/** The swap day count */

private static final String SWAP_DAY_COUNT = "ACT/365";

/** The swap interval */

private static final String SWAP_INTERVAL = "6M";

/** The curve day count */

private static final String CURVE_DAY_COUNT = "ACT/365";

/** The business day convention */

private static final String BDC = "Modified Following";

/** The spot date */

private static final LocalDate SPOT_DATE = LocalDate.of(2016, 10, 5);

/** The number of spot days */

private static final int SPOT_DAYS = 2;

/** The holidays */

private static final LocalDate[] HOLIDAYS = new LocalDate[] {LocalDate.of(2016, 8, 1)};

/** The calendar */

private static final Calendar CALENDAR =

new CalendarAdapter(new SimpleWorkingDayCalendar("Calendar", Arrays.asList(LocalDate.of(2016, 8, 1)), DayOfWeek.SATURDAY, DayOfWeek.SUNDAY));

/** The yield curve */

private static final ISDACompliantYieldCurve YIELD_CURVE;

static {

final ISDAInstrumentTypes[] instrumentTypes = new ISDAInstrumentTypes[] {

ISDAInstrumentTypes.MoneyMarket, ISDAInstrumentTypes.MoneyMarket, ISDAInstrumentTypes.MoneyMarket, ISDAInstrumentTypes.Swap,

ISDAInstrumentTypes.Swap, ISDAInstrumentTypes.Swap, ISDAInstrumentTypes.Swap, ISDAInstrumentTypes.Swap, ISDAInstrumentTypes.Swap,

ISDAInstrumentTypes.Swap};

final Period[] tenors = new Period[] {Period.ofMonths(3), Period.ofMonths(6), Period.ofMonths(9),

Period.ofYears(1), Period.ofYears(2), Period.ofYears(3), Period.ofYears(4), Period.ofYears(5), Period.ofYears(7),

Period.ofYears(10)};

final ISDACompliantYieldCurveBuild builder = new ISDACompliantYieldCurveBuild(TRADE_DATE, SPOT_DATE, instrumentTypes, tenors,

DayCountFactory.INSTANCE.instance(MONEY_MARKET_DAY_COUNT), DayCountFactory.INSTANCE.instance(SWAP_DAY_COUNT), Period.ofMonths(6),

DayCountFactory.INSTANCE.instance(CURVE_DAY_COUNT), BusinessDayConventionFactory.INSTANCE.instance(BDC),

CALENDAR);

CURVE = builder.build(QUOTES);

}

The curve is built from convention information (day-counts, payment intervals, etc.), a list of instruments used in the curve, the tenors of these instruments, a working day calendar, and market data. As conventions are defined on a per-currency basis, we are going to bundle all of the convention information into a class and then add functions that allow these objects to be constructed in Excel. This means that conventions can be stored in Excel tables.

The conventions

We’ve added two POJOs, and

that contain all of the convention information for yield curves and CDS, and a utility class,

, that contains static Excel functions that build these objects.

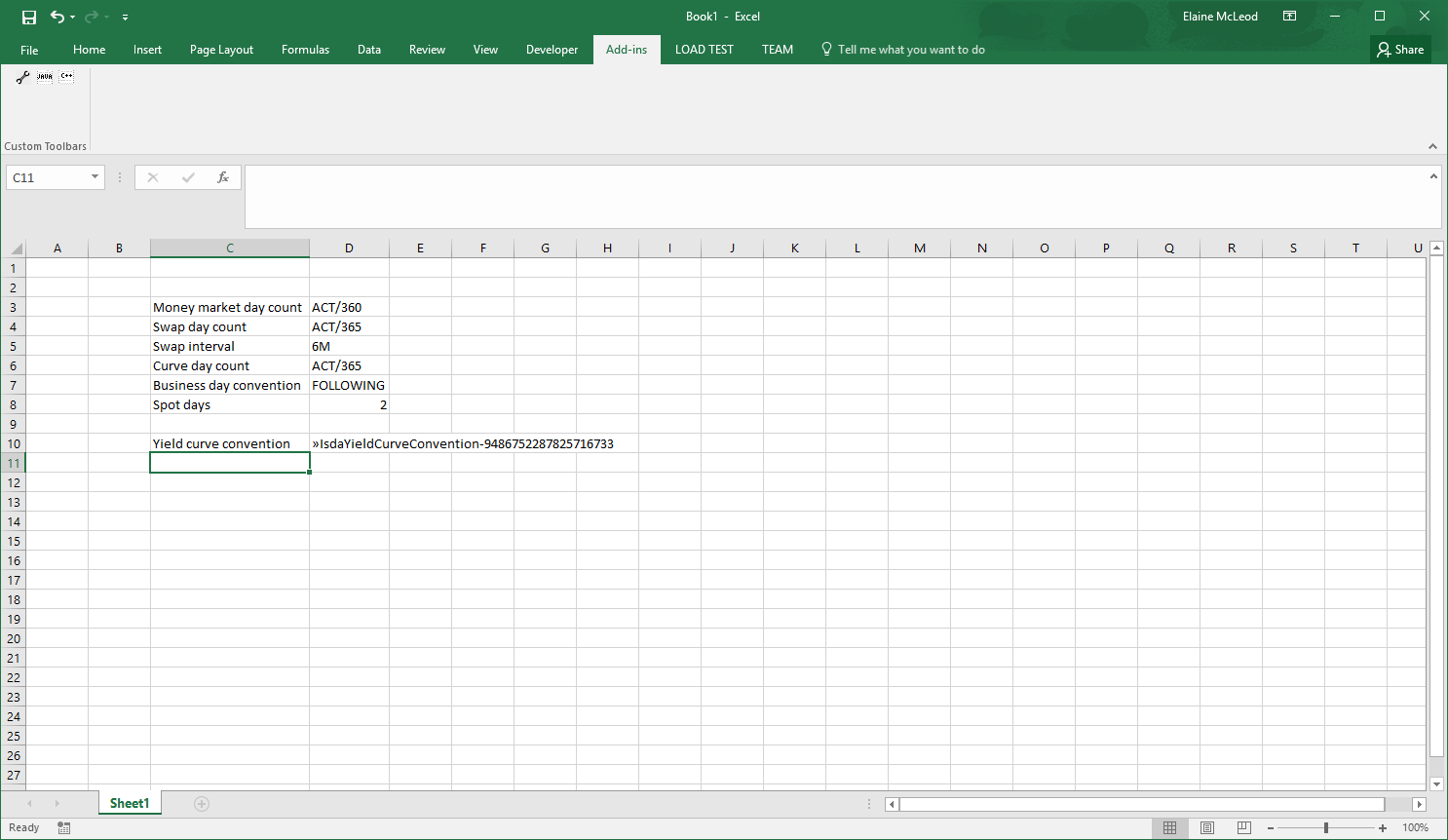

The yield curve convention builder is simple: all fields are required and can be represented as String or int.

This method takes Excel types (XLString, XLNumber) as arguments, which means that there is no type conversion done on the objects coming from the add-in.

@XLFunction(name = "ISDAYieldCurveConvention", category = "ISDA CDS model", description = "Create a yield curve convention")

public static IsdaYieldCurveConvention buildYieldCurveConvention(

@XLParameter(description = "Money Market Day Count", name = "Money Market Day Count") final XLString xlMoneyMarketDayCountName,

@XLParameter(description = "Swap Day Count", name = "Swap Day Count") final XLString xlSwapDayCountName,

@XLParameter(description = "Swap Interval", name = "Swap Interval") final XLString xlSwapIntervalName,

@XLParameter(description = "Curve Day Count", name = "Curve Day Count") final XLString xlCurveDayCountName,

@XLParameter(description = "Business Day Convention", name = "Business Day Convention") final XLString xlBusinessDayConventionName,

@XLParameter(description = "Spot Days", name = "spotDays") final XLNumber xlSpotDays) {

final DayCount moneyMarketDayCount = DayCountFactory.INSTANCE.instance(xlMoneyMarketDayCountName.getValue());

final DayCount swapDayCount = DayCountFactory.INSTANCE.instance(xlSwapDayCountName.getValue());

final DayCount curveDayCount = DayCountFactory.INSTANCE.instance(xlCurveDayCountName.getValue());

final BusinessDayConvention businessDayConvention = BusinessDayConventionFactory.INSTANCE.instance(xlBusinessDayConventionName.getValue());

final Period swapInterval = parsePeriod(xlSwapIntervalName.getValue());

return new IsdaYieldCurveConvention(moneyMarketDayCount, swapDayCount, swapInterval, curveDayCount, businessDayConvention, xlSpotDays.getAsInt());

}

The @XLFunction annotation means that this method is available from Excel. The fields are self-explanatory: the name of the function, a more detailed description and the category that the function will appear in. None of these properties are mandatory - the default value for the name is the method name, the class name for the category and an empty description if they are not filled in. There are other properties that will be discussed in more detail later. The @XLParameter properties have the same meaning as those in the function annotation.

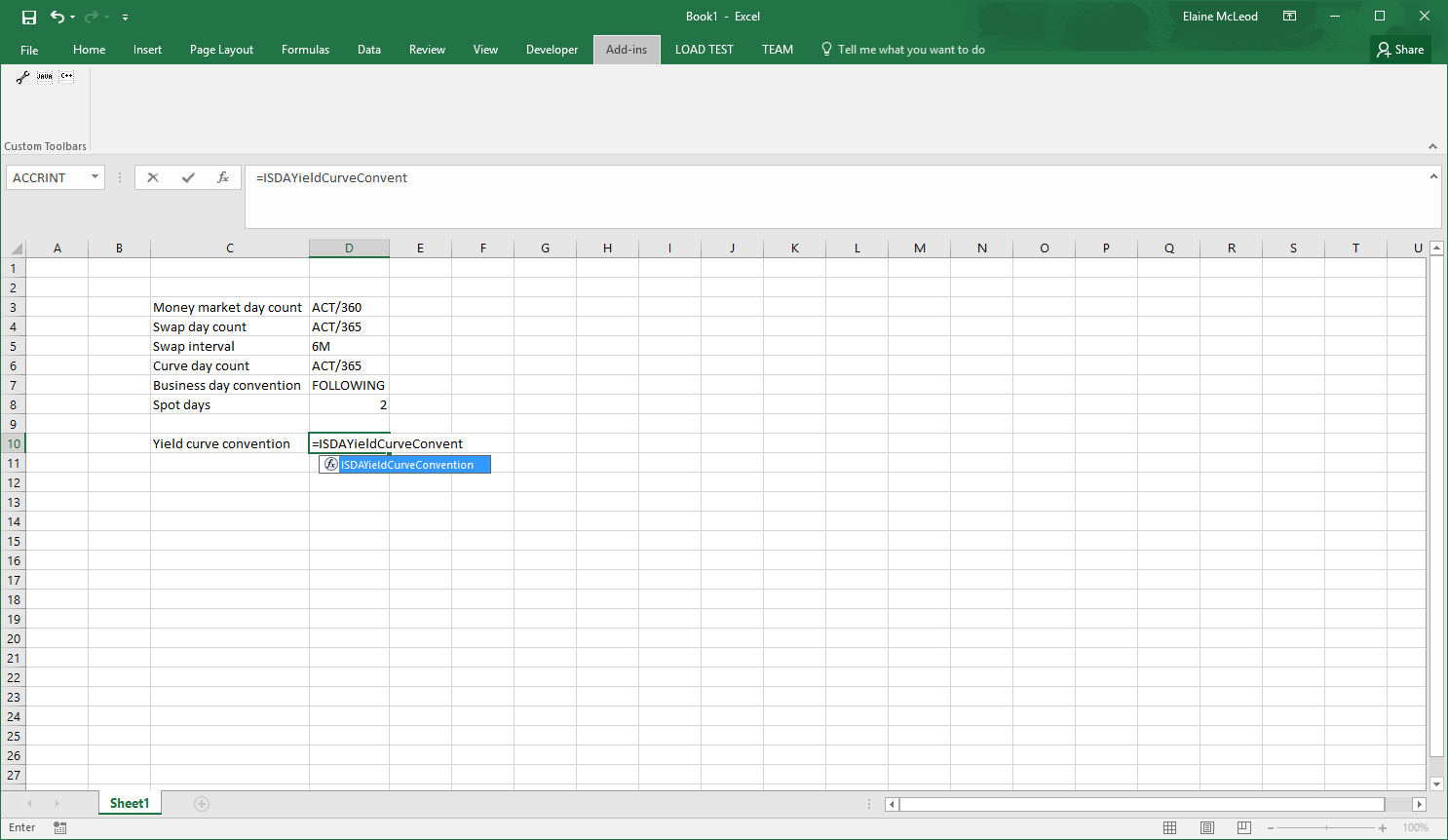

After this function is built, it can be called from Excel

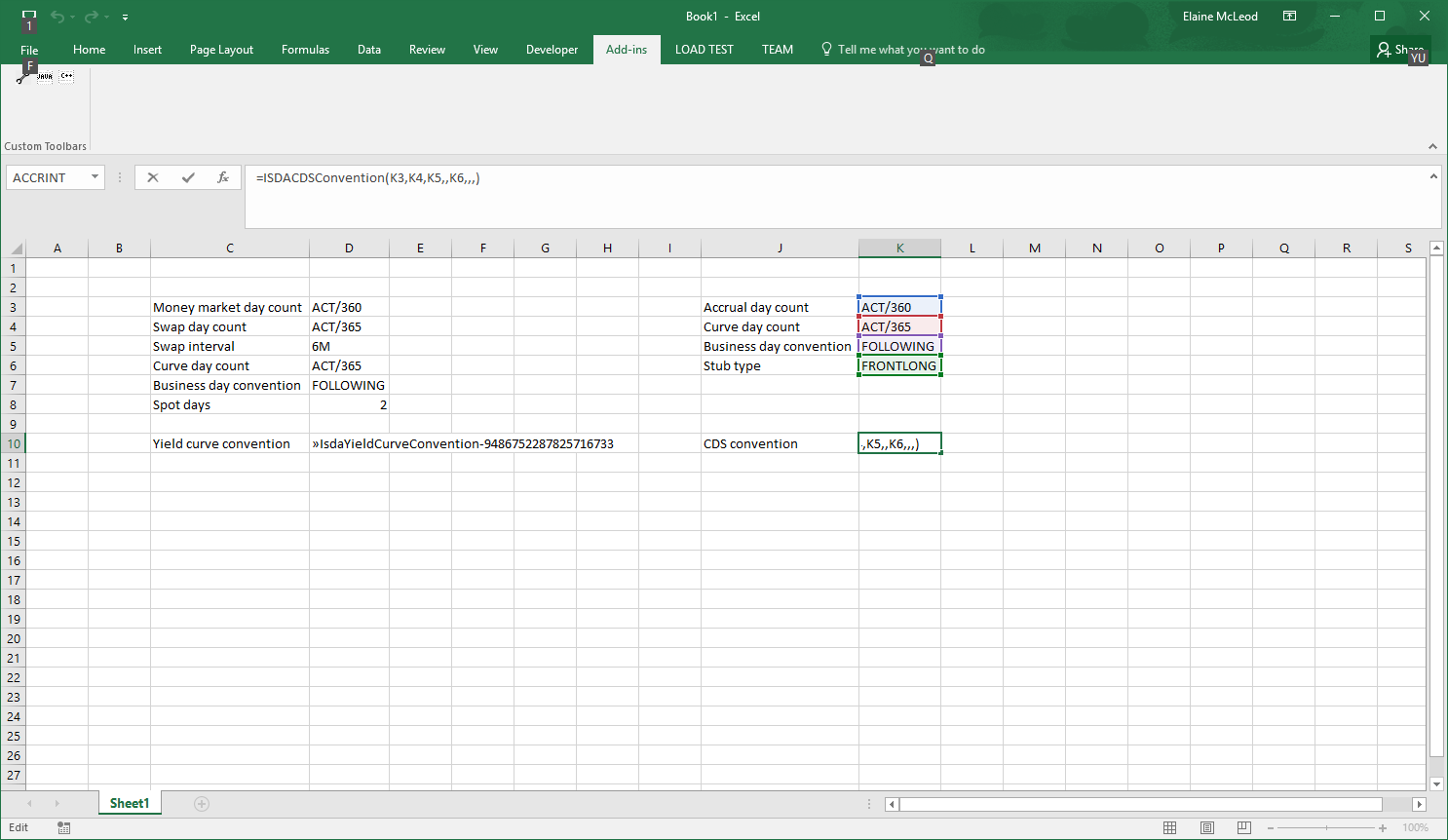

The CDS convention builder is very similar to the yield curve convention builder, but some fields are optional:

@XLFunction(name = "ISDACDSConvention", category = "ISDA CDS model", description = "Create a CDS convention")

public static IsdaCdsConvention buildCdsConvention(

@XLParameter(description = "Accrual Day Count", name = "Accrual Day Count") final XLString xlAccrualDayCountName,

@XLParameter(description = "Curve Day Count", name = "Curve Day Count") final XLString xlCurveDayCountName,

@XLParameter(description = "Business Day Convention", name = "Business Day Convention") final XLString xlBusinessDayConventionName,

@XLParameter(description = "Coupon Interval", name = "Coupon Interval", optional = true) final XLString xlCouponInterval,

@XLParameter(description = "Stub Type", name = "Stub Type", optional = true) final XLString xlStubType,

@XLParameter(description = "Cash Settlement Days", name = "Cash Settlement Days", optional = true) final XLNumber xlCashSettlementDays,

@XLParameter(description = "Step In Days", name = "Step In Days", optional = true) final XLNumber xlStepInDays,

@XLParameter(description = "Pay Accrual On Default", name = "Pay Accrual On Default", optional = true) final XLBoolean xlPayAccrualOnDefault) {

final String stubType = xlStubType == null ? null : xlStubType.getValue();

final Integer cashSettlementDays = xlCashSettlementDays == null ? null : xlCashSettlementDays.getAsInt();

final Integer stepInDays = xlStepInDays == null ? null : xlStepInDays.getAsInt();

final Boolean payAccrualOnDefault = xlPayAccrualOnDefault == null ? null : xlPayAccrualOnDefault.getValue();

return new IsdaCdsConvention(xlAccrualDayCountName.getValue(), xlCurveDayCountName.getValue(), xlBusinessDayConventionName.getValue(),

xlCouponInterval.getValue(), stubType, cashSettlementDays, stepInDays, payAccrualOnDefault);

}

As optional values are passed in as nulls, it’s necessary to test for them and handle appropriately. Optional values are dealt with in the usual Excel way by leaving the argument blank in the formula:

The next stage is to actually construct the yield and CDS curves. Again, the wrapper class has been written with various static methods that call into the starling code. For these methods, the arguments are standard Java objects (e.g. double[]) rather than XLValue, which means that type conversion is performed automatically. This means that we don’t have to think about how to deal with arrays (what if the data were passed in as a row? a column?), as well as cutting down on the boilerplate of unwrapping and casting these objects to the types that are needed.

@XLFunction(name = "ISDAYieldCurve.BuildCurveFromConvention", category = "ISDA CDS model",

description = "Build a yield curve using the ISDA methodology")

public static ISDACompliantYieldCurve buildYieldCurve(

@XLParameter(description = "Trade Date", name = "Trade Date") final LocalDate tradeDate,

@XLParameter(description = "Instrument Types", name = "Instrument Types") final String[] instrumentTypeNames,

@XLParameter(description = "Tenors", name = "Tenors") final String[] tenors,

@XLParameter(description = "Quotes", name = "Quotes") final double[] quotes,

@XLParameter(description = "Convention", name = "Convention") final IsdaYieldCurveConvention convention,

@XLParameter(description = "Spot Date", name = "Spot Date", optional = true) final LocalDate spotDate,

@XLParameter(description = "Holidays", name = "Holidays", optional = true) final LocalDate[] holidayDates) {

This class contains two methods that construct yield curves; one that takes a convention object and another that constructs the convention itself. Note that although the methods are overloaded in the Java code, as you’d expect, the names of the functions are different. All function names in Excel must be unique; if a function has already been registered with the name, this is logged and the function ignored.

## Starting from scratch

We’re going to build a sheet that takes historical time series data from , performs some basic statistical analysis and compares a long-only portfolio to the efficient frontier.

A prerequisite for any sort of time series analysis is to make sure that the data are clean (e.g. no spikes) and consistent across dates (i.e. all have the same dates with no missing values). To do this, we should at a minumum:

- Allow the time series to be sampled at a particular frequency e.g. daily or monthly

- Have the ability to pad the series when there is no data for a particular date

It is certainly possible to do these operations using only Excel and / or VBA. However, it’s easier write functions in Java to do this, with the added bonus that the resulting spreadsheet is smaller (10 years of daily data is ~2500 data points - that’s a lot of rows or columns to manage), which means, amongst other things, that any errors or problems like #VALUE! can be more easily spotted.

We start with a toy implementation that extends a

SortedMap. There’s a factory method that takes either a 2 x n or n x 2 range and returns the TimeSeries as an object:

@XLFunction(name = "TimeSeries",

description = "Create a time series",

category = "Time series",

typeConversionMode = TypeConversionMode.OBJECT_RESULT) // NOTE THE CONVERSION MODE

public static TimeSeries of(@XLParameter(name = "datesAndValues", description = "The dates and values") final XLValue... datesAndValues) {

ArgumentChecker.notNull(datesAndValues, "datesAndValues");

if (datesAndValues.length == 1 && datesAndValues[0] instanceof XLArray) {

return ofRange((XLArray) datesAndValues[0]);

} else if (datesAndValues.length == 2 && datesAndValues[0] instanceof XLArray && datesAndValues[1] instanceof XLArray) {

return of((XLArray) datesAndValues[0], (XLArray) datesAndValues[1]);

}

throw new XL4JRuntimeException("Cannot create time series from input");

}

The only difference between this function and the ones in the previous section is that the conversion mode for the results is set to OBJECT_RESULT. OBJECT_RESULT functions do not perform any conversions, so the sheet will show an object reference.

The default mode is SIMPLEST_RESULT, which performs conversions to Excel types (e.g. Double to XLNumber) where a converter is available, or returns an object reference for more complex types without converters, like ISDACompliantYieldCurve.

For this example, we will use functions with OBJECT_RESULT , as this will help with our stated aim of writing a compact spreadsheet.

We’ve also added a function that expands a time series to an Excel array:

@XLFunction(name = "ExpandTimeSeries",

description = "Expand a time series into an array",

category = "Time series",

typeConversionMode = TypeConversionMode.SIMPLEST_RESULT)

public static TimeSeries expand(@XLParameter(name = "timeSeries", description = "time series object") final TimeSeries timeSeries) {

return timeSeries;

}

At first, this function does not look like it does anything to the time series. However, note that the conversion mode is SIMPLEST_RESULT. If we add a class that converts , then the time series will be converted to an array that can be used like any array formula in Excel:

Next, we need functions that generate schedules, a sampling function that gets the dates and values from a time series for a particular schedule, functions that deal with missing data, return calculators and arithmetic operations. All of these classes are in the package.

One of these functions is a percentage return calculator:

@XLNamespace("TimeSeries.")

@XLFunctions(

prefix = "PercentageReturn",

typeConversionMode = TypeConversionMode.OBJECT_RESULT,

description = "Calculates the percentage return of a time series",

category = "Time Series")

public class PercentageReturnCalculator implements TimeSeriesFunction<TimeSeries> {

@Override

public TimeSeries apply(final TimeSeries ts) {

ArgumentChecker.notNull(ts, "ts");

final int n = ts.size();

ArgumentChecker.isTrue(n > 1, "Need more than one data point to calculate the returns");

final TimeSeries result = TimeSeries.newTimeSeries();

final Double[] previous = new Double[] { ts.get(ts.firstKey()) };

ts.entrySet().stream().skip(1L).forEach(e -> {

result.put(e.getKey(), e.getValue() / previous[0] - 1);

previous[0] = e.getValue();

});

return result;

}

}

There are two annotations that weren’t used in the other examples: XLNamespace and XLFunctions.

XLNamespace

As its name implies, this annotation allows functions to be categorised into namespaces by prepending the value of the annotation to all functions in a class. This can be very useful if you have a large number of functions, as they will be sorted alphabetically in a drop-down list.

XLFunctions

The XLFunctions annotation is used when you want to register all public constructors and methods, including static methods, in a class (with the exception of the methods from Object: hashCode, equals, toString, finalize, getClass, wait, notify, notifyAll and clone - if you need one of these methods then you’ll need to add an explicit XLFunction annotation to it).

The fields in this annotation are fairly straightforward:

prefixis an optional field that effectively renames a class. In thePercentageReturnCalculatorclass shown above, the prefix field is set toPercentageReturn. This means that the function name for the constructor isTimeSeries.PercentageReturn, while theapplymethod’s function name isTimeSeries.PercentageReturn.apply. If this field is not set, the class name is used instead (e.g. givingTimeSeries.PercentageReturnCalculatorandTimeSeries.PercentageReturnCalculator.apply).typeConversionModesets the return type mode of the methods in the class. By default, it is set to return the simplest result, which means that if there are any converters available for the return type they will be used.descriptionprovides the description of the constructors and methodscategoryputs all constructor and method functions into a particular category.

The registered functions for the percentage return calculator are:

Note that when the functions are registered, the visibility of the constructors or methods is not changed, so only public ones will be registered.

For a detailed description of all of the fields in the annotations that have been used, see the document.

The sample sheet

Using the functions that we’ve created, we can now put together our sheet. The Market Data sheet makes a call to Quandl for data and splits the TabularResult by field name:

The Statistics sheet uses the calculators that we’ve written to prepare the time series data:

and calculate some statistics:

Finally, the Efficient Frontier page uses some Java functions, such as the covariance matrix calculator:

inbuilt Excel functions:

and Solver

to calculate minimum risk portfolio weights for various target returns. Much more straightforward than writing your own minimiser in Java, or trying to keep track of 10 years of data in Excel!

## Using existing code (2)